Prologue

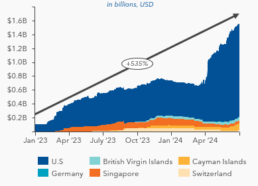

In April 2023, Franklin Templeton became the first issuer of U.S. registered mutual funds to be processed by a public blockchain, with the issuance of its OnChain U.S. Government Money Market Fund (FOBXX). FOBXX held the title of the largest tokenized U.S.-registered mutual fund up until late March 2024 when BlackRock launched its USD Institutional Digital Liquidity Fund (BUIDL). BlackRock leveraged the Ethereum blockchain to offer shares as tokens in the fund, offering instant settlement, enhanced liquidity, and a stable token value. These developments are part of a larger story of the accelerating growth of real-world asset (RWA) tokenization. Since January 2023, the tokenized government securities market in the U.S. alone has grown 10X, now valued at $1.6B (See Exhibit 1).

What is RWA Tokenization?

RWA tokenization refers to the digitalization and financialization of any tangible or non-tangible asset, ranging from financial products and trademarks, to real estate and collectible art. Put simply, it means the representation of a familiar asset (e.g., bond) as a token on a chain.

Currently estimated at $5B, the total addressable market for RWA tokenization is expected to exceed $15T over the next decade (a growth rate of ~300,000%).1

Of the $5B, 99% of tokenized assets are U.S. Treasury bonds, an attractive asset amidst an era of elevated bond yields.2

These tokenized bonds and money market funds not only facilitate faster processing with lower costs, but also offer unique benefits across the buy and sell side, democratizing access to capital and enhancing operational efficiency. So what does this mean for the future of capital markets, and how can players stay relevant amidst this change?

Exhibit 1. Asset Value of Tokenized Treasuries3

How does it work?

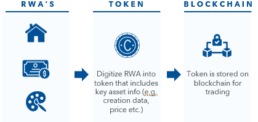

RWA tokens refers to an asset in digital form, combined with information and assignable digital rights, all connected in a programmable and automated manner. These tokens can represent parts or entire physical or intangible assets such as real estate, stocks, bonds, or art. This token exists on the blockchain and digitally represents the asset that can be easily traded. To purchase a token, a user does not need to have a bank account, credit card, or other financial products, leading to greater access to investments for people who are unbanked.4

The size of the prize

The explosive growth of RWA tokenization is largely driven by the coupling of the value of real-world assets with the attractive features of blockchain technology. With these features, described below, RWA tokenization is the key to unlocking the next chapter in capital markets.

1. EFFICIENCY

Tokenization of real-world assets generates efficiency gains across all stages of the asset trading value chain. For the sell side, the high cost of issuance and manual processes involved, particularly for corporate bonds, can be easily resolved by the automation of processes. For the buy side, the development of decentralized trading platforms can enable extended trading hours and accelerated clearing/settlement for tokenized assets.

2. LIQUIDITY

RWA tokenization not only facilitates efficiency gains, but also enhances asset pricing accuracy, enabling previously illiquid assets to be traded at much higher levels. In addition, the fractionalization of assets reduces barriers to entry for assets with historically high investment thresholds. These two levers, accurate asset pricing & asset fractionalization, enable access to capital, particularly for unbanked populations.

3. TRANSPARENCY

Tokenization can also enhance transparency of capital transactions, terms, and ownership. By storing tokens on a public blockchain, DLT trading platforms act as the single source of truth, intermediating the relationship between issuers and investors. For government debt securities, storing tokenized treasuries on a blockchain provides an immutable record of ownership, ensuring responsible usage and a clear distribution of asset yields and other benefits.

4. SAVINGS

The above features of RWA tokenization translate to large cost savings for the sell side. By removing manual processes and the need for intermediaries, asset issuers can streamline operational efficiencies, decrease backend costs, and reduce fees previously necessitated by asset compliance reporting, monitoring, and custody. Notably, tokenized bonds are estimated to reduce middle and back-office costs by 85%, or $15M for every $10B assets under management6, delivering savings via smart contracts and cross-border settlement. The use of distributed ledger technology (DLT) eliminates the hassle of cross-border boundaries, while smart contracts automate coupon payments, options execution, and other asset services often charged by central securities depositaries.

Exhibit 2. Tokenization Process5

Step 1: Establish Goals

DECODE CURRENT SYSTEMS AND CAPABILITIES

Start by conducting a comprehensive assessment of current systems and capabilities architecture. This involves mapping out the end-to-end process flow, identifying the teams involved, their responsibilities, and any overlaps across various teams. It is essential to consider which business units are involved and assess any limitations across the defined architecture. This assessment should include gathering requirements, not just from a technical perspective, but from all relevant areas, including business, governance, and implementation-specific needs. By identifying these baseline capabilities and requirements, organizations can create a clear foundation for the necessary changes in their transformation.

ESTIMATE TOTAL COST OF OWNERSHIP (TCO)

The current baseline extends beyond defining the architecture to mapping the entire ecosystem to it, with Total Cost of Ownership (TCO) playing a crucial role. TCO includes direct costs (systems, applications, tools) and indirect costs (employee time, downtime). Accurately assessing TCO for existing systems is vital to understanding the full financial impact. For example, a healthcare provider must consider both direct costs, like EHR licenses, and indirect costs, such as disruptions. This assessment helps compare current expenses with the benefits of new solutions, justifying investment in technological transformation.

Exhibit 3. HSBC Orion

Exhibit 4a. Existing Bond Lifecycle

Bonds: A case study

Debt securities, such as corporate bonds, are likely to dominate the tokenized market due to the sheer size of its underlying markets and benefits derived for tokenization. Exhibit 4a details the current processes and players involved in the existing bond lifecycle. Each phase is riddled with manual processes and pain points that could be addressed via tokenization as discussed below.

In contrast, tokenization allows for transparency and immutability of bond ownership as recorded on public blockchains, thereby reducing issuance costs and increasing issuance frequency.

1. BOND ISSUANCE

Bond bookbuilding, the process by which banks underwrite a bond, determines bond yields, maturity, and issuer financing needs. This process has undergone limited digitalization and consists of mostly manual processes, leading to higher fees charged by agents and increased barriers to entry for consumers.

2. PRIMARY & SECONDARY TRADING

Similarly, bond pricing discovery is a largely manual process, leading to pricing inefficiencies and fragmented liquidity. Liquidity is further exacerbated with restrictions on trading hours for investors. With the use of distributed ledger technology and tokenization, automation of asset servicing and trading means enhanced liquidity, extended or 24/7 trading hours, and immediate price discovery processes, and further reducing potential pricing inefficiencies.

3. CLEARING & SETTLEMENT

Until May 2024, clearing and settlement of U.S. bonds often took two business days by central clearing houses and security depositories (T+2). While the SEC has since mandated most bonds settle within one business day (T+1), extended clearing and settlement times nevertheless still pose risks for both buyer and sellers. Opaque, siloed data structures further exacerbate this process with manual reconciliation processes.

In contrast, tokenization and smart contracts enable accelerated settlement timeframes and reduce the risk of fraud and/or trade failures. DLT platforms combine asset & cash ledgers, reducing the need for central securities depositories (CSDs) to intermediate transactions.

4. ASSET SERVICING

Similarly, smart contracts automate the execution of post-trade corporate actions (e.g., collection of coupon payments). Previously managed by CSDs and custodians with unclear chains of custody and manual workflows, issuers of tokenized bonds can choose to automate asset servicing via new digital asset custodians.

In summary, bond tokenization can lead to significant efficiency gains, liquidity gains, and cost savings (see. Exhibit 4b). While there may be potential consolidation in existing roles and reduced revenue via intermediated fees, tokenization also enables increased revenues from more frequent bond issuances/transactions and creates opportunities for new players and digital asset revenue streams

Exhibit 4b. Tokenized Bond Lifecycle

A new capital markets value chain

Financial institutions, particularly banks, serve a central role in influencing the adoption of RWA tokenization, particularly for financial assets. In the context of asset wealth management, banks can play the role of issuers, digital facilitator, or custodians for their clients. As RWA tokenization reshapes the landscape of capital markets, commercial banks are well positioned to leverage their expansive reach and extensive infrastructure to set up synergetic partnerships with blockchain providers and adapt to new roles within the digital asset value chain. As financial institutions prepare to enter the world of RWA tokenization world, it is crucial to understand how traditional value chains may be impacted by tokenization and to make critical decisions to lay out the groundwork for success. These considerations include:

1. ASSET SUITABILITY & MARKET DEMAND

The first step towards tokenization is identifying which asset class to tokenize, ranging from real estate, commodities, and art to more traditional financial instruments such as bonds or equities. Factors such as asset liquidity, market demand, regulatory compliance, and valuation should be considered as part of this process. More importantly, financial institutions should consider how the tokenized asset may contribute to their overall growth strategy and identify potential synergies with their existing asset portfolio.

2. PARTNERSHIPS WITH TECHNOLOGY PROVIDERS

To prepare for asset tokenization, financial institutions should assess their current capabilities and identify gaps in their existing infrastructure. Partnerships with tokenization technology providers is the most common path towards addressing those gaps to facilitate tokenization. Financial institutions should assess the provider’s expertise, security protocols, compliance with regulatory standards, costs, and its ability to integrate with their existing tech stack to enable a smooth and secure tokenization process for both the bank and the consumer. Below are a few common technology providers that help banks engage in tokenization:

1.Alpha Point: Assists in RWA for banks, financial institutions, business, and government agencies

2.Securitize: Investment platform that helps institutional investors access private markets by tokenizing RWA

3.Polymath: Capital platform that allows banks to digitize RWAs

4.Bit Bond: Asset tokenization and digital asset technology provider that banks can user to create and manage tokens

5.TOKO Network: Digital asset creation platform to tokenize tangible or intangible assets

6.Vertalo: Private asset management platform that offers tokenization services

3. IMPACT OF TOKENIZATION ON BANKING

Tokenization is poised to change various aspects of the financial services value chain across the front, middle, and back offices. As a financial institution, awareness of which parts of your business are susceptible to change and the degree of the change can help prepare for the future of tokenization.

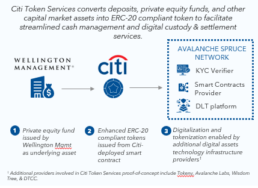

Exhibit 5. Citi Token Services

1. Front office: The degree of change might be highest in the types of financial products being offered as tokenized offerings are likely to require 24/7 market access, supporting operations, marketing / sales collateral, and a strong message on customer trust to ensure the tokenized solution is not to be confused with cryptocurrencies. Beyond products, a certain degree of change might be required for onboarding and compliance activities with the focus on tracking specific tokenized product usage and funding options to enable 24/7 trading. Tracking tokenized product usage may be necessary from a regulatory reporting perspective until the tech becomes more mainstream.

2. Middle office: The largest impact in the middle office might stem from the integration with the tech provider enabling on-chain transactions. As such, order management and trade execution functions will require integration with 3rd party solutions, including strict adherence to all current checks and balances while ordering of executing a trade (e.g. alignment to model guidelines, risk alerts, etc.). Continuing the theme of regulatory management, connecting data feeds to any internal compliance advisory, and tracking & monitoring solutions for post-trade activities is a must as well. The relatively easier integrations are to reporting systems to ensure that performance tracking, management reports, and any obligations to any special considerations (such as ESG tracking and reporting) are maintained as well

Exhibit 6. Impact of RWA Tokenization on the Asset Wealth Management Value Chain

3. Back office: The most likely change with a higher degree of impact in the back office is likely on data management, with backend systems that need to be integrated with the new tech vendor/s supporting tokenized trading. At the very least, these integrations will require transactions capture but can also extend to other contextual information about the trade that the financial services institution negotiates with the vendor (e.g., global pricing data at the time of the trade). Typically, these integrations will also need reports to be generated and provided in a certain format for existing backend systems to manage downstream workflows. Further, any special case analytics required to track tokenized asset trading might need to be layered on as well. Finally, any billing add-ons that are specific to tokenized asset trading would require feeds to the institution’s billing and revenue management platform.

Looking into the future...

The recent wave in RWA tokenization is set to transform the global exchange of value and information across global industries, and financial institutions are uniquely positioned to leverage its growth.

RWA tokenization isn’t just a phase, but an inevitable evolution for capital markets:

- Tokenization creates efficiency gains throughout the entire asset trading value chain by automating issuance and manual processes for the sell side and enabling extended trading hours and faster clearing/settlement for the buy side.

- Improved pricing accuracy and asset fractionalization enable greater trading volume for previously illiquid assets and reduce investor barriers to entry for assets with high investing thresholds, democratizing access to capital.

- DLT-enabled trading significantly lowers asset issuance, but may impact the economics of the issuance value chain by reducing legal and custody costs through the automation of services via smart contracts

These benefits not only help to explain the rapid growth of RWA tokenization, but also point to a future where all capital assets are tokenized and transacted on the blockchain.

Traditional financial institutions, particularly investment and commercial banks must take advantage of the rapidly improving blockchain technologies.

Commercial banks are uniquely positioned to leverage their expansive reach and extensive infrastructure to garner synergetic partnerships with blockchain providers and adapt to new roles within the digital asset value chain.

1-2. DefiLlama

3. RWA.XYZ

4. Roland Berger

5. Outlier Ventures

6. CashLink