INTRODUCTION

Over the past few years, Blockchain has promised to revolutionize business with its potential to transform diverse industries. Blockchain’s impact on the business world is projected to grow to $176 billion by 2025. B2B industries like banking, healthcare, insurance, and retail are only some of those that stand to benefit from the application of blockchain alongside smart contracts – a set of rules and policies that governs transactional agreements hosted on a blockchain network.

B2B finance is growing; in payments, B2B cross-border transactions constituted 80% of total cross-border transaction volume in 2015 and have been growing ever since. A large portion of these cross-border B2B transactions are sent via wire transfers today: 69% of businesses used wire transfer for cross-border payments in 2019. The need for speed and security in this space is well established and has only been exacerbated by the pandemic.

In insurance, openIDL, a network built on the IBM Blockchain Platform with the American Association of Insurance Services (AAIS) is automating insurance regulatory reporting and streamlining compliance requirements, thus improving efficiency and accuracy. In the energy industry, smart contracts are efficiently governing the distribution of energy in microgrids.

Devices in a microgrid are linked by smart sensors enabled by the internet of things (IoT) which monitor energy usage and reduce unnecessary energy distribution while generating smart contracts based on the consumer’s real-time usage.

HOW IS BLOCKCHAIN TRANSFORMING B2B

Blockchain is emerging as a game changer for several B2B sectors. It can securely transmit remittance data along with payments in cross-border B2B transactions. Through real-time tracking of products, blockchain helps reduce fraud and error, identify issues faster, and eliminate paperwork in supply chain alongside accelerating purchase order management and payment settlement. Blockchain-enabled lending could eliminate intermediaries and enhance security. Lastly, it allows customers to track, trace, transfer, and redeem loyalty points in real-time.

Exhibit 1.Blockchain Use Cases

1. Cross-border Transactions

Automation and technologies like blockchain are gaining momentum with several card networks and payment processing firms offering solutions that can boost security and reduce transaction times. Blockchain-enabled cross-border transactions are expected to grow at 117% between 2018 and 2023 with value of cross-border transactions recorded on the blockchain expected to cross $4.4 T by 2024.

Exhibit 2.X-border payment in traditional vs Blockchain

Traditional forms of global payments infrastructure move money from one payment system to another through a series of internal book transfers across financial institutions. If Company A in the United States wants to pay Company B in India, Company A asks its US bank to send a payment overseas. The US bank partners with a correspondent bank to facilitate the transfer, and a respondent bank in India receives the funds and then transfers it to Company B’s bank account (see exhibit 2).

These transactions tend to be expensive and inefficient due to cumbersome processes with multiple middlemen involved charging fees for processing of each transaction. According to Ripple’s analysis, $1.6 trillion us spent in systemwide costs for global cross-border transactions. Settlement of these transactions takes as long as 2-5 days.

They tend to be opaque since real time account status is hard to track and the cost is hard to predict as banks make deductions about which the payer is uninformed. Additionally, these transactions are unsecure since records are kept by one central authority like a bank, who is vulnerable to interference and error rates that run upwards of 12.7 percent.

Blockchain stands to revolutionize B2B cross-border payments by solving these challenges through streamlining the process and storing every transaction in a secure distributed ledger. Blockchain has proven to be cost effective and immediate since B2B payments with blockchain result in a 40-80% reduction in transaction costs and take an average of four to six seconds to finalize transactions.

Furthermore, these transactions are transparent and secure since as a decentralized ledger, it holds a verifiable and irreversible record of every transaction and distributes it for all authorized users.

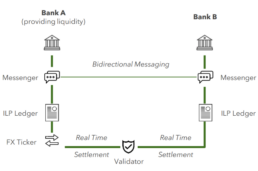

Several players operate in the blockchain-enabled cross-border payment space. Ripple’s growing global network includes 12 of the top 50 global banks. Ripple’s xCurrent is solving the messaging and settlement problem that exists in the financial system. It allows for real-time messaging and settlement between banks (see exhibit 3). Santander is building a payment corridor that would let customers in Latin America send money to the US via One Pay FX, a mobile app that uses Ripple’s xCurrent software. Other examples include that of MoneyGram, PNC Bank, and Standard Chartered.

Exhibit 3.Ripple’s xCurrent

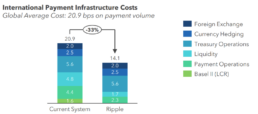

Exhibit 4. International Transaction Costs

✓ Messenger: provides communication between RippleNet members regarding risk and compliance, fees, FX rates, payment details, etc.

✓ Validator: used to cryptographically confirm the success/failure of transaction and to coordinate moving of funds across ILP.

✓ ILP Ledger: used to track credits, debits, and liquidity. Enables funds settlement atomically; transactions can settle instantly or not at all.

✓ FX Ticker: facilitates the exchange between ILP Ledgers by enabling liquidity providers to post FX rates.

Ripple’s xCurrent can reduce cross-border payment cost by 33% (see exhibit 4). Other examples include that of Mastercard and Visa. Mastercard and R3 (a leading enterprise blockchain software provider which includes 300+ financial services firms, technology companies, central banks, regulators, and trade associations) entered a strategic partnership to develop and pilot a new blockchain-enabled cross-border payments solution that will initially focus on connecting global faster payments infrastructures, schemes, and banks supported by a clearing and settlement network operated by Mastercard.

2. Supply Chain Management

Supply chains currently experience several challenges. Most supply chains rely heavily on manual processes making it time-consuming and costly to trace back products in the chain. Each year worldwide, unsafe food products cause 600 million cases of foodborne diseases. To trace these issues back the source, it can take up to weeks. Several major food-borne bacteria outbreaks, several recently in the US, are encouraging increasingly more companies to investigate blockchain as a new method for increasing visibility and traceability of the goods.

Blockchain-enabled supply chain ensures increased supply chain speed since digital track record allows for real time status update into the end-to-end supply chain. Recording product status at each step on blockchain makes it possible to trace each product to its source and helps eliminate waste generated by manual handling of paperwork. Walmart created a food traceability system based on Hyperledger Fabric, the open-source ledger technology. By placing a supply chain on the Blockchain, it allows making the process more transparent and traceable; it can now trace the origin of over 25 products from 5 different suppliers (see exhibit 5).

A UK-based company – Blockverify is helping pharma companies track and trace end-to-end supply chain of medicines i.e., origination details, factory and processing data, expiration dates, storage temperatures and shipping detail to identify counterfeit products and verify product authenticity and reducing tracing time to mere 2.2 seconds!

Exhibit 5.Blockchain Powered Supply Chain

3. Procure-to-Pay

Another related popular use case for blockchain in B2B is procure-to-pay. Procure-to-Pay (PTP) is the multi-step process connecting clients with their multiple service providers. It not only allows for identification of service providers, but also involves the complex process of quality check and invoicing and payment settlement. Current state of P2P process and solutions involve multiple middlemen, limits transparency, and is prone to errors.

▪ Manual processes: When an order is released, it goes through manual approvals (including online e-signatures). The process of collecting purchase order (PO), goods receipt (GR) and invoice takes days because of multiple manual intervention and physical checks at each point.

▪ Limited visibility: Opaque supply chain limits any transparency into spend, products, and risk ratings of the vendor.

▪ Delayed payments: Payments often get stuck in a series of approval processes and validation of receipts. Blockchain can disrupt procure-to-pay by generating sustainable cost reductions, efficiency improvement, fraud control and transparency enhancement.

▪ Enhanced transparency: Blockchain enables creation of a single source of truth (SSOT) about products in a supply chain via a global ledger. Each product has its own entry on the blockchain that can be tracked back to its raw materials.

▪ Low risk vendor selection: Since risk rating is on blockchain, every time an organization wants to do business with a supplier, they would go to the blockchain platform and look for the history of performance of the supplier. Since the information on blockchain in immutable, organizations will feel confident that the date is not tampered with.

▪ Accelerated purchase order management: Purchase order and good receipt data would be exchanged on the blockchain at an accelerated pace, in addition to helping identify the nearest and best in class vendor within the network. This would in turn reduce time to search vendor and process purchase orders and receipts.

▪ Quality check: Since all product/service specifications are stored on blockchain and updated in real time, it is significantly easier to perform quality check against set pre-agreed upon standards.

▪ Faster settlements: Blockchain-powered smart contracts automate the transfer of ownership of the goods and authorize the release of payments if the quality check meets the required specifications. There is no reconciliation required between PO, GR, and Invoice because every transaction is already approved between the parties in blockchain. This ensures that settlement time is reduced significantly; from ~30 days to seconds.

▪ Streamlined complaint/enquiry addressing: Due to high transparency into the supply chain all the way back to raw materials, any enquiry about any component is easily addressed.

One such blockchain powered PTP solution is B2P by R3 built on Corda Blockchain. It is integrated with existing ERP systems of an organization so that the PO and GR can be managed through B2P platform. It automatically matches and verifies POs, GRs and invoices and participants can track the status of approval and payment in real-time.

4. Lending and Financial Risk Management

A traditional lending process requires high involvement of

intermediaries like loan officer, banks, underwriter, and loan processors, which could drive costs and inefficiencies. Additionally, loan applications could take a couple of weeks and the rate of interests differ widely around the world. Using blockchain in lending could help remove intermediaries from current system.

▪ Cost Reduction: Blockchain could reduce the costs by allowing the borrowers to deal with lenders directly

▪ Secure: By removing the need for gatekeepers in the loan and credit industry, blockchain technology can make it more secure to borrow money and provide lower interest rates.

▪ KYC and Fraud Prevention: By storing customer information on decentralized blocks, blockchain technology can make it easier and safer to share information between financial institutions.

Blockchain technology opens up the possibility of peer-to-peer (P2P) loans. Companies like SALT Lending, Lendoit, and Jibrel Network have launched a P2P lending platform using blockchain and smart contracts. One such lending platform is HashLend where visitors can register either as lenders or borrowers. Borrowers can make the payments using smart contracts embedded with a crypto wallet. If a borrower does not pay installments timely, the smart contract could add late fees to the actual amount and upgrade it on the ledger.

Exhibit 6. Blockchain-enabled lending

5. Trade Finance

Trade finance is a centuries old industry that has not seen much innovation. With approximately 80-90% of world trade relying on trade finance, the influence of blockchain on the market would be felt globally throughout all industries that use cross-border trading.

Current state of trade finance involves multiple challenges:

▪ Manual contract creation: The import bank manually reviews the financial agreement provided by the importer and sends financials to the correspondent bank

▪ Invoice factoring: Exporters use invoices to achieve short-term financing from multiple banks, adding additional risk in the event the delivery of goods fails

▪ Delayed payment: Multiple intermediaries must verify funds delivery to the importer as agreed

▪ Multiple versions of truth: As financials are sent from one entity to another, significant version control challenges exist as changes are made/complete

▪ Multiple platforms: Since each party across countries operates on different platforms, miscommunication is common and the propensity for fraud is high

Exhibit 7. Trade finance consortia

Blockchain brings several benefits for trade finance:

▪ Removed need for paper reconciliation since all parties are linked on the platform and updates are instantaneous

▪ Quick turnaround allows unlocking liquidity for businesses

▪ Transparent factoring: Invoices accessed on Blockchain provide a real-time and transparent view into subsequent short-term financing

▪ Automated settlement and reduced transaction fees: Contract terms executed via smart contract eliminate the need for correspondent banks and additional transaction fees

6. Loyalty Programs

Loyalty programs are of utmost importance to not only for customer retention but also for attracting new customers and deepen share-of-wallets. Use case of blockchain in loyalty rewards programs ensures that loyalty reward program providers, administrators, system managers, and customers interact in one system without intermediaries.

A highly insightful of target state loyalty program in the blockchain world would be one involving several partners (e.g., credit card companies, airlines, hotels, e-commerce, etc.). Upon purchasing airline tickets with credit card, the airline and the credit card company simultaneously credit loyalty tokens to the loyalty rewards wallet in real-time instead of these points residing in separate loyalty accounts that must be accessed and redeemed in separate platforms. Additionally, these points can be used for redemption at the hotel or any other loyalty program partner as opposed to waiting days to redeem these points on separate platforms.

Exhibit 8. Single and transparent platform for loyalty points

Exhibit 9. Real-time credit and redemption of points

Furthermore, healthcare and insurance companies who incentivize their customers to take care of their health by crediting points for achieving targets like step count, completing preventative health check-up, etc. could leverage blockchain for real-time loyalty credit transfer. For example, upon completion of target steps in a week tracked by smart watch, customer gets points which could be redeemed for a free smoothie at a partner café and lower premium amount (see exhibit 9).

Such real-time transparency can enhance customer experience, offer new ways to interact with customers, and would result in cost savings in the medium to long run.

IN CONCLUSION..

Blockchain is not so much a strategic choice as it is a necessity for capturing unique business opportunities and customer experiences.

For realizing its benefits, companies must:

▪ Set up identify the best use cases

▪ Partner with the right ecosystem of capability providers and advisors

▪ Leverage existing infrastructure (i.e., distributed ledger platform

protocols and standards like those created by Ethereum)

▪ Develop multi-year transformation roadmap for medium-to-long run

(i.e., business case, implementation timelines)

1. Gartner; Forecast: Blockchain Business Value, Worldwide, 2017-2030

2. Global Payments 2015: A Healthy Industry Confronts Disruption

3. Pymnts; Deep Dive: Why Businesses Are Seeking New Technologies To Optimize Cross-Border B2B Payments During The Pandemic

4.Juniper Research; Blockchain: Key Vertical Opportunities, Trends & Challenges 2019-2030

5.Ripple: The Cost-Cutting Case for Banks, 2016

6.Ripple: The Cost-Cutting Case for Banks, 2016

7.LeewayHertz