CUSTOMER AWARENESS IS ON THE RISE

Economic, climatic, demographic and technological shifts around the world are (re)shaping markets and client expectations continuously. For example, when forest fires rage across continents of Europe and America, an investor asks her advisor to invest her money in assets that have sustainability at the core of their value proposition. She doesn’t stop there; she asks her advisor to provide her with evidentiary support for claims made by these investment opportunities. These conversations on thematic/ goal-based investments were uncommon a decade or two ago when climate change was not threatening our future generations at today’s scale.

The forces above have also produced the new-age tech-savvy mass affluent millennial investor. This investor looks to manage her money the same way she shops, socializes, communicates and learns — leveraging worldwide resources, with no geographic limitations. These shifts will have major implications for wealth advisors, who will need to adapt.

In this paper, we review some of the biggest changes impacting the go-forward opportunities for wealth advisory firms.

OPPORTUNITY# 1 | OPEN WEALTH

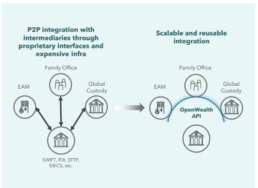

In December 2020, delegates from the asset management industry met in Switzerland and reached an agreement on adopting communally shared APIs. This led to the birth of Open Wealth which aims to define, maintain and operationalize open API standards for the global wealth management community.

Exhibit 1. Transition to Open Wealth APIs

The creation of this standard catalog of common APIs will serve several use cases, including:

1. Automated sharing and consumption of customer data, KYC and documents with and from custody banks

2. Real time reconciliation of securities positions

3. Digital triggering of transactions and updates to client profiles

Such APIs are expected to significantly reduce development and operational expenses as well as implementation timelines for asset managers and custodians. A few ways in which these efficiencies will materialize include:

1.Higher efficiency in custody banking/services

a. Position and transaction data for reconciliation on real-time basis

b. Integration with different CRMs to automate client onboarding (customer data and KYC documents)

2.Innovative ecosystem-based business models

a. Platform-based ecosystem and business models

b.Data-driven cost efficiencies in custody services arising from data aggregated from other banks

3. Reduction in Risk

a. Reduction of operational risk through process automation

b.Reduction of regulatory risk through secure and real-time exchange of client data shared across networks

The adoption of these standards will also enable innovative, low cost and user-friendly wealth management offerings.

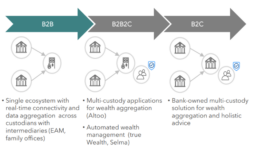

Exhibit 2. Evolution from B2B to B2C

OPPORTUNITY# 2 | VERIFIABLE IMPACT INVESTING

According to Cerulli Associates, the intergenerational wealth transfer will set in motion a change of ownership of $84 trillion of wealth between now and 2045, making millennials the primary base of investors in the future.

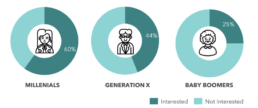

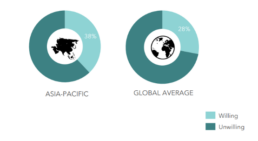

Exhibit 3. Desire to move to Sustainable Investments

According to Morgan Stanley, 86% of millennials are interested in sustainable investing. As a result, many large asset managers, including BlackRock, are announcing initiatives that put sustainability at the center of their investment strategy.

The core idea behind verifiable impact investing (VII) is to find new sources of alpha from robust and trusted Impact opportunities. It allows firms to issue investment tokens directly linked to verified data.

These tokens are made available to investors who gain access to new and trusted sources of alpha.

Distributed Ledger Technology (DLT2) enables the transfer of value to Small and Medium Enterprises and creates an immutable record of the transaction. As the tokens are updated with new information, an asset manager can monitor and report on the investment.

At present, 95% of impact investors identify collecting data on investment products and opportunities as challenging, indicating a whitespace between supply and demand for opportunities. Early examples of investment platforms have emerged demonstrating benefits from data trade-offs.

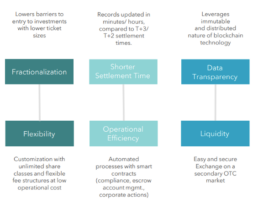

Exhibit 4. Tokenization

*Impact tokens contribute to the UN SDGs, often representing a specific impact in the form of a

measurement metric such as several vaccinations or gallons of drinking water and providing proof

delivery of positive impact

Moeda is a cooperative investment platform whose core proposition is to connect investors directly with small businesses fostering UN sustainable development goals. It overcomes the challenges of traditional funding by utilizing the ability of digital tokens to crowdsource funding.

Veridium Labs is trying to solve the trading of carbon offset credits in the open market. It seeks to measure the carbon impact of a product through the entire supply chain. For this, it creates a digital token that acts as a layer on top of the carbon credit to give it a value in terms of “carbon density per dollar times product group”. This measurable value of impact allows investors to identify companies that meet sustainability goals.

Additional benefits of VII will include:

1. Opening new investment opportunities that would have incurred significant search and validation costs for an asset manager

2. Mitigation of investment risk through robust verification of investment data

OPPORTUNITY# 3 | CONVERGENCE

Even though the mass affluents constitute over one-third of the number of adults across the globe, wealth managers continue to chase and serve the HNWI/UHNWI, letting go of the lucrative opportunity at hand. (Refer to Exhibit 5)

Exhibit 5. Distribution of Investors by Wealth (2021)

The Mass Affluent cohort alone drives more than $230bn of revenue. Additionally, its wealth has been growing both organically and through inheritance, raising demands for more sophisticated services and advice. At present, it is highly underserved with only 15-20%4 of this segment being serviced.

With democratization of access to the full range of investment opportunities through tokenization, digitization of services, and availability of investment information, the needs of the various wealth segments have been converging. This convergence now spans across investment profile, customer experience and service demand. Consequently, wealth managers can very cost effectively target multiple segments with minimum service differentiation.

Investment profile

The asset classes sought by mass affluent and high-net-worth individuals have converged over time. While the mass segment portfolio has traditionally comprised ETFs and mutual funds, it has now diversified into alternatives. This section has been able to expand its search for higher returns due to the fractionalization of investments through tokens.

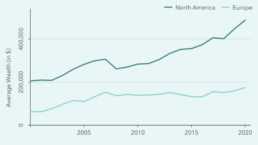

Exhibit 6. Individual Wealth is on the Rise

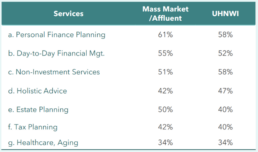

Exhibit 7. Service Demand – Mass Affluent Vs. Uhnw

Advisory service

While high-net-worth individuals continue to demand advice related to personal finance and financial management, the mass affluent have caught on to this demand. They present an equal, if not greater interest in services such as day-to-day financial advice, tax advisory, estate planning, etc. (refer to Exhibit 7).

Customer experience

With digital engagement becoming the norm, the mass affluent segment can be targeted without extra effort, since similar capabilities are needed for HNWIs and UNHWIs. Investors irrespective of wealth holdings are looking to modify their interactions through an optimal mix of digital and in-person communication.

OPPORTUNITY# 4 | IOT AND DIGITAL TWINS

Ranging from everyday voice services like Alexa to robots that move products around factory floors, the Internet of Things (IoT) has continued to take giant strides.

This market is estimated to reach $650B in 2026. Subsequently, the amount of data generated by IoT devices is expected to grow four times from 2019 to 2025 (to 73 ZB).

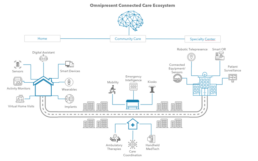

These stacks of information lay the foundation for developing digital twins (virtual replicas of physical infrastructure and customers) which utilize real-time data and AI techniques to optimize performance and forecast actions.

For wealth managers, IoT also opens multiple avenues to serve customers better. For example, the geo-location of investors can be referred to a local advisor with calendars optimized for the best use of time. In addition, through Open Finance, information on clients’ finances can be aggregated to ascertain whether there is enough for daily expenses, liquid savings and long-term investments. The IoT-digital twin promotes the use of customer data to simulate the behavior and provide personalized products and services to suit specific preferences and needs. (Refer to Exhibit 9)

For example, a digital twin of the investor can be used to focus on improving customer fulfilment via online channels by creating simulations of interactions and developing virtual assistants that optimize the business flow of interacting with customers.

Vitality, an insurance provider, combined smart technology tracking healthy behavior with investment rewards in stocks, shares and ISAs.

Their healthy living discount reduced monthly product charge which encouraged savers to look after their health. Additionally, customers with insurance policy plans paid discounted charges if they engaged in healthy living program and invested in Vitality funds. In another application, a digital twin of a built asset can be constructed

to help screen and manage risks, improve asset value and capital allocation process. A city-level digital twin for the Cross River Rail in Australia was created to support investment decisions. It helped accommodate different types of investors and their investment strategies, including PE firms, commercial banks and institutional

investors.

Digital twins can be extended to represent a range of assets. This could vary from low-yield, low-risk core assets like energy and water to newer asset types such as data centers, air or seaport expansion.

IoT’s application in wealth management is largely untapped today. It provides a significant opportunity for a deeper customization of investment strategy using behavioral data and drive greater engagement with an investor’s finances.

Exhibit 8. China & North America will see exponential growth in IOT

Exhibit 9. Use Cases for IOT and Digital Twins

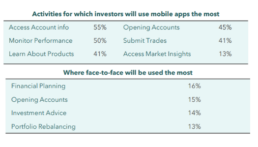

Exhibit 10. Preference Between Physical And Online Interaction Across Activities

OPPORTUNITY# 5 | FRONT OFFICE DIGITALIZATION

Digital servicing of customers has increased significantly with the global pandemic, accelerating its adoption across industries. Within wealth management, face-to-face investment advice has been supplemented with digital advice for overall service delivery. Experience reveals that face-to-face interaction remains crucial in certain aspects and it helps foster deeper investor engagement and confidence. (Refer to Exhibit Investor needs are diverse – refer to exhibit 11) with some preferring robo-advisors that facilitate investments round-the-clock and others delegating the management of assets to an investment professional.

The preference for channels ranges from mobile applications demanded by younger mass affluent investors to UHNW investors expecting dedicated human advisors along with digital services. The overarching need remains constant, i.e., to be provided with investment ideas that are relevant to the individual’s specific portfolio at that moment rather than one-size-fits-all recommendations.

OPPORTUNITY# 6 | THE GREAT WEALTH TRANSFER

The wealth industry will be significantly impacted by the Great Wealth Transfer to Millennials. An estimated $84 trillion will shift from baby boomers to Generation X and millennials between now and 2045, with 80% of heirs expected to find a new advisor once they inherit.

In preparation for this wealth transfer, it would be beneficial for wealth managers to follow a holistic strategy, which includes:

1. Profiling the average millennial customer (See Exhibit 12)

2. Modifying service channels, service offerings and products

3. Creating multidisciplinary teams that address the financial wishes of multiple generations

Exhibit 12.Wealth Management Needs And Profile Of Millennials

In terms of transforming service offerings and products,

▪ Wealth managers can offer discounted services for pooled family assets to incentivize the next generation of wealth holders

▪ Older businesses, especially established family offices, can choose to partner with wealth tech to offer digitally native service offerings

▪ Millennial investment preferences can be met by offering specific products, such as goal-based investment accounts, inclusionary investing and ESG investing.

However, for long term retention of customer base, it is imperative that wealth managers who are used to serving individuals, shift their business models and address the family as a whole as their customer.

For example, integrated financial planning can place emphasis on strategic estate planning that not only ensures that generational wealth is preserved instead of being lost to estate taxes but also brings in a client’s heir into the conversation before they inherit.

Exhibit 13. Opportunities To Transform Wealth Services

OPPORTUNITY# 7 | RISE IN FAMILY OFFICES

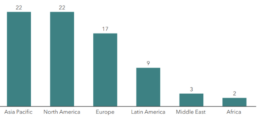

Exhibit 14. HNWI Holdings, By Region (US$ Tr)

With millennials standing to gain from the Great Wealth Transfer, a greater emphasis on purpose and sustainability will be made in investment decisions. This second generation of investors also presents a higher appetite for risk and a willingness to experiment with alternative assets like cryptocurrency and NFTs. (Refer to Exhibit 15)

To be successful it is imperative for wealth managers to master the A-Z of this industry, from tax structures to ESG and globalization needs of the investors, strategically through a mix of in-house and outsourced capabilities. Raffles, an Asian family office recently collaborated with Huobi Tech to introduce cryptocurrency-based investments in its offerings.

Exhibit 15. Willingness To Invest In New Asset Classes

Traditionally, simplicity and confidentiality drove decisions but with the increasing wealth and complexity of structures, institutionalization of wealth through family offices has taken the front seat. To succeed family offices should be focusing on:

– Understanding the unique family structures

– Delivering tailor-made solutions

– Reviewing and updating solutions regularly

The surge in family offices not only indicates economic prosperity but also a need for greater expertise in smoothly running these complex structures. The demand for family office services far exceeds the supply, this talent shortage could force bidding wars amongst the interested parties. Outsourcing capabilities by exploring the OCIO path (Outsourced Chief Investment Officer) where assets are managed by third-party experts that have efficient systems for managing middle and back-office tasks can prove to be beneficial.

A few examples include The Coury Firm which expanded its OCIO services to serve small to medium-sized foundations and single-family offices and Purple, an asset management firm which sits in Singapore but serves across Asia, the Middle East and Europe.

OPPORTUNITY# 8 | DEMOCRATIZING ALTERNATIVES

The world of alternative assets is diversifying at a fast pace with new-age alternatives attracting investor interest over “traditional” alternatives. Not only are the investment options multiplying, but also the investors seeking to benefit from these options such as “the mass affluent”.

With the financial crisis of 2008, retail investors have sought to diversify their investments away from traditional assets and tap into the potential of alternatives. Making this class of assets more accessible at lower risk to smaller investors has led to innovations in the concept of partial ownership of assets.

Tokenization attempts to create fractional digital shares of assets like Wine (Vinovest) or artwork (Masterworks), which could broaden access to alternatives for individual investors as well as create new opportunities for asset managers. Additionally, it could offer access to new types of assets, such as sneakers, comic books, revenues from sports teams, and other investments rarely available to mass investors.

A report by BNP Asset management, CAIA, and Liquefy argues that opening private assets to new pools of investors could finance needs over the next 20 years, including an estimated $15 trillion for global infrastructure. Fueled by this democratization, CAIA Association members expect allocation to alternative assets to rise to 18-24% of the global asset market by 2023.

Exhibit 16. Tokenization In Alternatives

In Closing...

While advice has always remained at the core of wealth management, finding the balance between human and digital advice has become vital to remain relevant in the forthcoming years. The incoming wave of younger customers, growth in the number of high-net-worth individuals, and increased internet penetration call for the industry to move from traditional assets and portfolios to alternative assets and hyper-personalized portfolios.

Wealth managers need to rethink their offerings and be creative in their products to keep the new entrants hooked, whether through shock-tech integrated watches or tokenization of wine, all while keeping an eye on the ever-growing stress on impact investing. The wealth management industry foresees dramatic changes in the value proposition and services, with wealth advisors soon embracing technology as a tool, and goal-based investing as an essential. The next big challenge is the lack of transparency in pricing and competitive fees. While firms figure out how to tackle these upcoming roadblocks to retain and entertain clients, open wealth, tokenization, and digital twins, terms off-lately considered distant, continue to become a norm and technologies, such as chatbots, IoT, and AI, fortify the growth of the industry.

1.Exhibit 3

2. DLT Definition

3.Capgemini World Report Series 2022

4.Citywire Asia

5.Thoughtlab: Wealth and asset management 4.0

6. Roland Berger Reports

7. Growth of IOT Devices

8. Statista

9. Redtail Advisorcomms Survey

10. The Economist

11. 2021 Global Family Office Report