The Growth Imperative

The past few years have brought about significant changes in the insurance industry. With the rise of digital-first consumers and advancements in technology, the industry has had to evolve to catch up with customer expectations. The adoption of newer technologies has enabled insurers to provide more personalized and on-demand solutions to customers, enhancing the overall customer experience. Generative AI, such as ChatGPT, is now transforming how insurers interact with their customers. From creating personalized content to running complex code, helping insurers streamline their operations and offer better services.

According to Gartner, by 2025, 75% of all insurance operations will be conducted using AI, ML, and IoT, compared to just 10% in 2019. If utilized to their fullest potential, these technologies can lower costs by 10-15% and grow revenue by 15-20%.

Thus, streamlining the bottom line is no longer enough. Insurers must rethink lead generation, agent interactions, and the way they service customers.

Exhibit 1. Exacting the next phase of growth

Seamless Phygital Customer Acquisition

Today customers research protection offerings through web reviews, social media, etc., in conjunction with advice from an agent. The preferred journey has moved beyond traditional agent interactions and now includes mobile phones, AI assistants and embedded interactions as well. Thus, insurers need to rethink customer acquisition strategies and build seamless on-off early engagement experiences.

With 67% of consumers ready to switch insurers after one bad experience(2), it is time for insurers to go “fully phygital”, creating a crack-proof digital-to-physical experience, vital to entertain and retain today’s digital consumers.

The insurance buying journey has gone online for a majority, that go offline only to seek advice when making the final decision or for solving complex queries, thus necessitating providing an end-to-end phygital experience :

Exhibit 2. Purchasing insurance through digital channels(1)

1. Research and Purchase Decision:

As a customer starts their journey by searching online, insurers should be ready with a user-friendly app and website with easy-to-find information about their offering along with a strong social media presence. The website can include virtual assistants to answer questions and offer online quote tools to allow customers to get a quick estimate of their premiums. Insurance content can be pushed via gamification, simplifying complex policies while educating the customers. Such game-based rewards can nudge them into sharing relevant information, referring products further, and receiving further communications and offers across platforms. (Exhibit 3)

As customers navigate through digital platforms, the agents should be notified about the customer’s requests so that they can seamlessly modify quotes, answer queries and revert by text or call with personalized options for the customer to finalize decisions while getting the right advice from the live agent.

2. Onboarding:

Once the policy is purchased, digital onboarding should be offered through a mobile app or website with document uploading functionalities, e-signatures, and digitally delivered welcome kits.

Insurance agents should be updated in real-time on the progress made by the customer on the onboarding front so that they can guide them through the process in case of roadblocks without asking preliminary questions when customers contact help desks or set up in-person meetings.

3. Policy Management:

During the course of the policy, customers can be provided with a portal to change or update coverage, pay premiums, explore other policies, etc.

Agents with the customers’ profiles and purchases can easily educate them on their purchased policies and plans or guide them through choosing appropriate ones.

4. Claims Processing:

Customers are provided with an option to file the FNOL online along with options to submit damage proof, track the status of claims, etc.

Agents can help in physical claims filing with personalized support.

Since a traditional insurance policy can get complex, agent involvement is necessary throughout the customer’s lifecycle. This necessitates a traditional-digital hybrid model, and only insurers able to balance digital and agent interactions will have an edge with future generations.

Exhibit 3. Phygital, Research, and Purchase process

Lead with Bite Sized Offerings

As insurers work on building a smooth omnichannel experience and adding new customer touchpoints, the focus should also be on exploiting these channels to expand the customer base and fulfill a larger set of the customer’s needs.

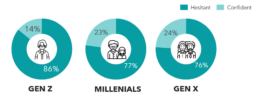

Today, most Americans across generations worry about buying life insurance or other high-ticket policies, as it is an important long-term financial safety net (Exhibit 4). This presents a unique opportunity for US insurers to incorporate bite-sized products into their product portfolio and nurture the relationship to bigger ticket products later.

Exhibit 4. Hesitation in Buying Life Insurance(3)

With customers being 5x more likely to buy additional insurance from an initial bite-sized insurer4, these insurance policies lay the foundation of a trusting relationship, while also providing a perfect entry point for customers who can’t afford or fully understand the more comprehensive policies.

This “lead-gen insurance” can be sold through easily-accessible digital touchpoints, covering specialized insurance at smaller premiums to reach a larger customer base. Various firms have introduced bite-sized offerings including SNACK a Life Insurer in Singapore that enables customers to accumulate Term Life, Critical Illness and Personal Accident insurance coverage using public transportation, completing step goals, dining at select restaurants, and paying micro premiums with each trigger. Similarly, SmallTicket in Korea primarily sells pet life & health insurance, but also offers travel insurance on an hourly/trip basis, protecting riders against accidental deaths and injuries.

Such bite-sized products can help insurers reach today’s task-rich, time-poor consumers. Additionally, sales are further boosted by fulfilling needs unmet by traditional large-ticket insurance policies while also:

Targeting underserved-upcoming markets such as the younger generation who are starting out in their careers and don’t have a lot of disposable income to spend on insurance, but may be interested in affordable, targeted policies like rental insurance or travel insurance.

Upselling and cross-selling larger policies such as selling a customer a small travel insurance, and then using that relationship to offer them other types of insurance, like medical and life insurance.

Simplifying customer experience by offering an easy-to-purchase, low-on-T&C interface attracting more customers and building loyalty.

Driving sales through data by utilizing AI to target ‘ideal’ customer segments (millennials, price-conscious individuals, travelers, etc.) through optimal channels (social media, mobile apps, direct marketing, or through bundling with other products and services).

Meeting Customers Where They Are

Embedded insurance isn’t a new concept, but a plethora of new use cases have sprouted over the years. Today customers are looking to simplify all aspects of living. Thus, purchasing insurance needs to be simpler than purchasing a pair of jeans from Amazon.

Examples of embedded insurance include:

i. Accident insurance with a full-day ski pass

ii. Dental insurance with dental kits

iii. Family life insurance or child life coverage while buying a crib

Though traditionally sold through direct or digital channels, and recently through third-party sites, the sales cycle for complex embedded insurance products should be reimagined by seamlessly embedding Agents into the buying experience. This way the conversation about protection is only natural. Agents can be guided by cross-sell and upsell recommendation engines that tailor the conversation with the customer based on their past behavior.

For example, an agent can initiate a conversation about health insurance with a customer purchasing travel insurance from a travel website. However, agent intervention is not needed for simpler products such as mobile screen insurance.

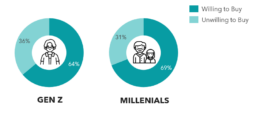

Over the years, customers have gotten accustomed to embedded P&C insurance. They now seem ready to accept it beyond P&C (Exhibit 5). Embedded insurance is estimated to make up 40% of total insurance sales by 2040(5).

Exhibit 5. Increasing Acceptance of Embedded Insurance(6)

Additionally, with the help of AI, insurers can further improve embedded services e.g., through dynamic pricing. Here, policies are priced based on real-time market changes and the customer’s risk tolerance, shifting from the traditional set-in-stone rule-based engines. This way insurers can maximize conversion probability i.e., quote optimal rates in seconds at the point of decision.

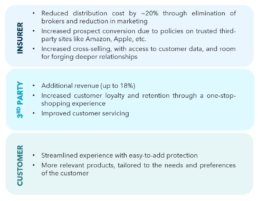

A well-thought-out embedded insurance experience can benefit all parties:

AI-gents

AI alone cannot reliably generate leads, convert them, or drive customer satisfaction since customers themselves continue to entrust advisors when making major life decisions such as buying the right insurance policy. Thus, the AI’s speed, consistency and cost-effectiveness should augment the agent’s relationships, experience and empathy to create a truly harmonized AI-gent, helping shorten turn-around time and increase customer satisfaction.

Exhibit 6. Aiding Advisors with AI

Quicker Redressal Through Chatbots

As social platforms change the way people communicate, customers now expect a quicker, more efficient resolution to their queries and to interact with an entity familiar with their journey to date. Customers are getting impatient and slow response time can be the deal breaker when making a policy-related decision. (Exhibit 7 & 8)

Enhancing customer experiences can drive growth of 4-8%. With the introduction of generative AI, insurers can now boost customer satisfaction through personalized responses to queries and assisting agents and customer care personnel quickly search large databases when solving complex claims or answering policy-related questions.

With an estimated savings of $80B by 20269, integration of AI into the customer service segment can:

Provide 24/7 Support: Using Chatbots, messaging apps and voice chat assistants that are mobile optimized

Reduce response times: External databases can be utilized to respond swiftly to complex queries, hold meaningful discussions, and determine when human intervention is necessary

Provide personalized recommendations: Using data from past queries and search history on channels customers interact with daily

Exhibit 7. Reasons for customer frustration (%) (7)

Exhibit 8. Customer Expectations with Query Response (8)

(Reducing customer patience across communication channels)

Solve unstructured asks and queries: With OCR and NLP techniques in place free text communications can be structured and simplified

Improve reach: Through multilingual capabilities

Manage Frauds: Fueled with machine learning and deep learning, AI solutions can identify recurring patterns of unusual customer behavior and run background checks before onboarding or accepting applications

Automate time-consuming tasks: NLP can automate pre-call, in-call, and post-call activities like after-call documentation, agent coaching, and summarization

Boost Marketing efforts: Response rates on various platforms and interaction analytics can identify preferences, common pain points and opportunities which can boost customer retention and build an ideal customer profile

Hyper-personalization

Generative AI is one such capability that can support multiple use cases throughout the journey.

Digital Experience: Today, the customer’s experience is largely dependent on the skills of marketers and agents. In a world of generative AI, traditional methods of customer segmentation and personas are no longer needed. Generative AI can target customers more precisely based on the information available and produce personalized messages on a case-to-case basis, handle email exchanges with customers along with generating website content, blog posts, etc.

Generative AI can also provide real-time feedback to agents on calls, summarize discussions, suggest next steps, and more.

Personalized Insurance Plans: Tailored fit policies can be designed without agent involvement using Generative AI and NLP tools that can consider lifestyle, employment, and health data extracted from policies, claims, conversation history, etc. Such policies that can cover customers unique asks to lead to greater satisfaction and retention

Underwriting: Vast amounts of data can be analyzed to generate personalized risk assessments based on a customer’s individual characteristics and circumstances. This also helps insurers identify risk factors that may not be apparent through traditional methods. Insurers can now also offer dynamic pricing based on driving data, claims history, etc.

Engagement and Retention: Predictive models can be used to anticipate the customer’s future needs and preferences. This can help insurers offer tailored coverage options that meet a customer’s unique circumstances, resulting in a more relevant experience, and boosting loyalty and stickiness.

Additionally, data from IoT devices, such as wearables and health monitoring systems, can be used to create personalized life insurance products that consider the customer’s specific health risks and needs. ML algorithms can also be used to analyze customers’ health records and family medical history to create customized life insurance policies that cover specific risks.

Exhibit 9. How generative AI can enhance the customer experience

Exhibit 10. Opportunities to hyper-personalize

In Closing...

In the current environment, streamlining the bottom line is no longer enough for US insurers. To find the next wave of growth, insurers must rethink lead generation, agent interactions, and the way they service customers.

Today’s must-haves for every insurer include — seamless phygital experiences, leading with bite-sized offerings, meeting customers where they are, AI-augmented agents, rapid redressals through chatbots, and hyper-personalization of products and experiences.

While these concepts are not new, they require aggressive deployment of AI/ML and a fundamental redesign of business processes and the underlying operating model. For example, traditional use of customer segmentation, mass-customization, and customer personas are no longer relevant in a world of generative AI.

The upcoming decade belongs to insurers who can pivot to this new model quickly!

__________________________________________________________________________________________________________

- Industry Outlook 2021

- IIR

- Nerdwallet

- Accenture

- IBM

- DrabikDigest

- Inbenta

- Aircall.io

Read More

The Open Book on Compliance – US Open Banking Regulations Decoded

The CFPB’s new Open Banking regulations will impact how financial service providers can access and monetize consumer data, while also influencing future practices around security, consent, and data sharing.

Mixed Reality

As these technologies become more accessible to the wider public, AR and VR are expected to grow into a $125 billion market by 2025.

Money Games

The use of gamification has proliferated across all industries, with retail, entertainment and education leading the charge. Apps like Duo Lingo, Kahoot, Fitbit, Starbucks etc., are all some of the most prevalent examples.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

From Cards to Chains – Payments in the Blockchain Era

To remain competitive in the evolving financial landscape, card networks are uniquely positioned to bridge this gap between traditional payments and new blockchain networks as transaction facilitators, leveraging their global reach to make transactions on their networks quicker, cheaper, and more secure.

A Borderless World

Significant shifts are underway in the cross-border payments sector, across the demand-side and supply-side. Consumer expectations from domestic payments (instant, fully traceable, risk-free, etc.) are being applied to the more complex cross-border space. Businesses that capitalize on these shifts stand to shape the future of the industry.

Cracking the FedNow Code

Real-time payments are increasingly recognized as a critical component of modern financial systems, offering speed and convenience in an interconnected digital world. As we venture into the future, the recent launch of the Federal Reserve's instant payment service, FedNow, stands at the forefront of a payment revolution in the US.

Future-Proofing Healthcare Delivery

The right telehealth platform is critical to meeting patient expectations and providing the best possible provider, patient and administrator experience. Today patients are demanding more control over their healthcare and want to access care from anywhere.

The GenZ Wave

Gen Z is not merely a younger version of millennials; they are poised to disrupt all aspects of the economy. Companies must therefore adapt in time to cater to the preferences and expectations.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The role of Value Added Resellers (VARs) is transforming from basic reselling to strategic technology partnerships that offer comprehensive IT solutions. To maximize the value of these evolving relationships, firms must bring transparency to pricing, agreements, and the scope of work.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Leading B2B firms are very well aware that their client delivery experience needs to have the same levels of service, responsiveness, transactional ease as any digital consumer experience. Majority (72%) of B2B buyers expect a similar experience on a B2B site as they get on a consumer website (1).

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Client Loyalty 2.0

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.