Wave of Platformization

Platformization has emerged as a pivotal trend, particularly in highly fragmented sectors such as healthcare, which features over 4,000 software vendors.(1) Healthcare organizations are often so fragmented, it is not unusual for companies to need 300+ isolated point solutions for their day-to-day processes.(2) This proliferation of apps significantly increases the need for integrations, all while IT budgets become more constrained from multiple subscriptions to different point solutions.

Across industries, large technology firms such as Salesforce, ServiceNow, and Workday are responding to this need for consolidation and leading the wave of platformization through strategic acquisitions and rapid development. For instance, Salesforce has developed features for customer engagement and servicing, employee collaboration, and analytics into a single solution. This shift has prompted companies across sectors such as Spotify, Humana, and Royal Bank of Canada to migrate to Salesforce, resulting in a 40% increase in sales productivity.(3) Similarly, ServiceNow offers a comprehensive IT Asset Management platform, streamlining everything from asset onboarding to cost management. Additionally, Workday consolidates human resource functions, providing integrated services in human capital and talent management, enhancing efficiency and reducing vendor complexity.

With these consolidated platforms, organizations are able to achieve greater synergies and interoperability for an all-in-all easier to use, more comprehensive system. This expansion of offerings has occurred over time to create a cloud-first, modern, customizable, and integrated system for end-to-end processes.

Exhibit 1. Evolution of Platforms

The Disjointed Healthcare System

While significant progress has been made, healthcare remains hindered by outdated and fragmented systems.

1. INSURERS

–For example, regional payers processing over 5 million medical claims annually use about 5+ vendors for claims adjudication alone. This is often supported by 50 additional vendors for other services such as file transfers, payment processing, and more.(4)

–Another payer manages over 2 million medical claims but restricts their all-in-one vendor to only two functions (e.g., claims processing and utilization management). However, they rely on custom-built solutions for other needs.(4)

Maintaining a fragmented system dramatically increases IT costs for claims processing, with the cost being 250% higher than more modern, integrated solutions. Additionally, to manage these systems, organizations often require 80% more personnel than industry norms.(4)

2. PROVIDERS

–On the provider side, many healthcare systems operate with 10-20 essential functions, such as administration and clinical operations, but are burdened from using hundreds of different systems to support all processes.

Driven by the burden of managing hundreds of vendors and the corresponding costs of doing so, healthcare organizations should be compelled to modernize and streamline their technology ecosystems.

Exhibit 2. Case for Platformization

Ripple Effects of Silos

The impact of siloed systems used in the healthcare industry extends widely, significantly affecting operational efficiency. Here’s how:

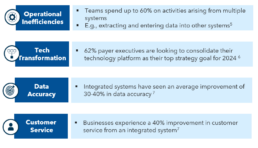

1. Data Fragmentation: Disconnected systems across different departments create data silos, hindering access and leading to outdated, duplicated data. Managing outdated and duplicated data costs 30% of total labor expenses, risks 4% of revenue in compliance, and further reduces revenue through inefficiencies.(8)

2. Tech Incompatibility: Using multiple vendors often requires a foundational connectivity layer. Established vendors often provide ready-made connections, whereas lesser-known vendors might require expensive custom builds to ensure compatibility. This can delay timelines and pose risks, with one in six companies reporting projects running 70% over schedule and 200% over budget.(9) This is particularly troubling for healthcare where compliance and strict deadlines outlined by regulators (e.g., CMS and state Medicaid) must be followed, or payers risk losing member contracts.

3. Manual Intervention: With so many systems, users are required to manually transfer and re-enter data across different platforms. This is not only time-consuming and error-prone, but also delays critical business decisions. Evidence suggests that organizations face annual losses of over $3 million if over 50% of a full-time employee’s workload is spent manually coordinating between systems.(10)

4. Resource Drain and Productivity Losses: Using many point solutions requires a larger technical staff dedicated to ongoing system integration and forces business professionals to focus on workarounds rather than their primary duties. Consequently, each new system update or technology introduction increases workload, stress, operational costs, and diminishes productivity.

5. Compromised Security: Each integration or communication layer adds a potential entry point for attacks, increasing the risk of compromised system security.

6. Limited Scalability: Fragmented infrastructure, data silos, manual processes, and a lack of standardization hinder the ability to scale technology. This is particularly problematic in healthcare, where growing patient and claims volumes demand robust, scalable systems.

7. Regulatory Non-Compliance: Data fragmentation and inconsistencies create incomplete audit trails, risking non-compliance with regulatory standards. Inconsistent data security protocols across various vendors can expose systems to cyberattacks, jeopardizing patient data and potentially resulting in costly HIPAA fines ranging from $100 to $50 thousand per violation(11).

8. Rise of Additional Vendors: Healthcare organizations frequently engage professional services to develop workflows and manage data fragmentation, leading to increased costs and increasing the number of vendors in the ecosystem.

Future of Connected Healthcare

Fragmentation persists both within and across payer and provider systems, affecting operations from core to surrounding segments. For payers, navigating the complex interdependencies of the value chain and the numerous entities involved, as detailed in Exhibit 3, is a nightmare in the absence of Platformization. For example, in insurance, the claims teams often manually inputs prior authorization data, constructs custom workflows to share finalized claims with state regulators and more.

These stopgap measures contribute to delays and a cascade of problems such as coding errors, repeated manual adjustments, and processing inaccuracies, leading to penalties upwards of $3 million9, elongated processing times, and lower auto-adjudication rates. Even for providers, a lack of a centralized source for patient data combined with no downstream connectivity with payer systems can lead to oversights in patient care. Vendors are actively consolidating systems and processes both across and within payer and provider domains to mitigate these issues. However, adoption rates for such solutions are still sub-optimal.

Exhibit 3. Payer Value Chain(12)

Exhibit 4. Modular Platformization of Healthcare

Consolidation efforts on integrating previously siloed functions, as demonstrated in exhibit 3, into fully configurable modules detailed in exhibit 4 are visible across vendors of various sizes and archetypes. For example, prominent ‘Pega-shops’ are leveraging their technological expertise and scalability to undertake comprehensive in-house custom builds. Players are also investing in acquisitions to expand scope of offering. For example, Oracle’s Health Insurance Cloud’s recent acquisition of Cerner, a leading EHR, showcases its expansion into both payer and provider domains.

Similarly, major professional services providers are acquiring companies to offer integrated products with adaptable modules, as illustrated by Cognizant’s acquisition of TriZetto. Even smaller professional services firms that started off as consultants for patching operational gaps, are now broadening their offerings to include consolidated healthcare products. Moreover, providers like Epic Systems, traditionally known for their EHR systems, are venturing into payer solutions, adding functionalities such as portals, enrollment, authorization, and utilization management tools.

Embracing Integrated Solutions

Integrated solutions can help organizations experience cost savings, data integrity, and a unified user experience.

1. Cost Savings: From a reduced number of licenses, streamlined maintenance and support, minimized training across different platforms, and simplified vendor management, organizations can experience significant cost savings.

2. Increased Data Integrity: As a result of one vendor, a “source of truth” with standardized data formats helps to decrease data silos and the need for manual entry into multiple systems.

3. Unified User Experience: A single interface across various process steps reduces the need to switch between systems and search for missing or outdated information, leading to a more unified user experience.

4. Single Point of Accountability: With one vendor, challenging scenarios such as system downtimes can be resolved quicker with the need to only work with that vendor. Additionally, using a broader range of services from a single vendor can strengthen relationships, which is vital for timely issue resolution.

Beyond the immediate benefits outlined above, there are substantial long-term benefits to be gained from establishing a strong partnership.

In healthcare, where platform procurement is a long-term commitment, it is essential for organizations to look beyond immediate financial benefits and choose a partner that not only supports but also actively guides their growth journey.

Below is how organizations should think of long-term partnership gains:

1. Premium Customer Support: Utilizing a broader array of services from a single vendor often leads to higher quality support. When one vendor is familiar with most of your operations, it can more easily identify issues. This also gives the organization greater influence over improvements and enhancements.

2. AI Leverage: Vendors continually invest to enhance their offerings. By adopting consolidated platforms, organizations can capitalize on vendors’ AI investments, which often include pre-built AI models and robotic processing automation. This comprehensive approach allows for more extensive improvements across the entire value chain, rather than just parts of it.

3. Pre-Built Market Integrations: Vendors that expand through consolidation often provide pre-built market integrations for areas of the value chain they have not ventured into yet that organizations can benefit from.

Still Not Foolproof

The choice to transition to a consolidated platform is not straightforward. Despite the potential benefits, adoption by both payers and providers remains measured.

1. Data Migration Issues: Point solutions often result in fragmented, non-standardized data. As a result, migration can be a daunting task. Furthermore, healthcare data is subject to strict privacy, security, and confidentiality regulations under HIPAA that organizations must adhere to during migration.

2. Vendor Lock-In: With a single vendor, organizations are heavily dependent on it for support, updates, and maintenance. If the vendor experiences issues (e.g., software, security), it can be extremely disruptive to the organization. However, these issues are rather rare and be combatted by baking in strong contractual terms.

3. Parallel System Maintenance: Migrating to a modern system often necessitates running old and new systems concurrently, leading to temporary high costs and increased employee workload from managing dual systems alongside their regular duties. To mitigate this, organizations need to plan and allocate resources accordingly.

4. Stringent Timeline: Payers must pay attention to the timing of their system migration. Insurers need to consider Medicare/Medicaid bid years, as regulators prefer to award business to organizations that are not in the middle of changing their technology stack.

5. Resistance to Change: Even with fragmented systems, users often grow comfortable with the wraparounds and manual inputs. Users often develop a resistant mindset, even if the change is to a more friendly system. Successful platform integration requires comprehensive change management, including extensive training and post-implementation support.

Even if organizations can mitigate these issues, consolidated platforms are not foolproof yet.

6. Ever-Evolving: Some platforms are still evolving in terms of configurability, breadth of offerings, integration capabilities and more. Because consolidation is a newer concept, many vendors are still working out the kinks and are not infallible.

7. Narrow Client Base: Vendors often face difficulties in establishing trust as some platforms are yet to secure a robust healthcare client base. Consequently, their operational experience is limited to a narrow range of plan types and geographic areas.

8. Vendor Oversight: Some platforms prioritize strategic acquisitions over thorough integration and testing. This approach often results in solutions that perform poorly, with vendors opting to cover up these deficiencies by acquiring additional technologies and organizations rather than addressing underlying problems. To mitigate this, it is important to thoroughly research vendors when choosing to switch systems.

In Closing...

Healthcare organizations must harness the momentum of platforms, embracing unified solutions that may still be evolving. This proactive approach is critical, allowing both organizations and vendors to ‘learn by doing,’ facilitating mutual growth. Benefits extend beyond cost savings, paving the way for establishing long-term relationships with vendors. Simultaneously, it enables vendors to refine and bolster their offerings in collaboration with a variety of healthcare entities.

Given the substantial investment required for such transitions, selecting the right vendor is important. Organizations should assess their needs, timelines, budgets, and the broader market context. Additionally, in these large-scale, high-stakes implementations, it is essential to identify requirements and establish robust contractual agreements as it would ensure mitigating the risk of ‘laying all eggs in one basket’.

__________________________________________________________________________________________________________

- Software Analyst, 2023

- Workato

- Salesforce: Automation keeps Spotify’s Ad Business Growing Year over Year

- Kepler Cannon analysis

- Harvard Business Review: What’s Lost When Data Systems Don’t Communicate, 2023

- 20Becker’s Payer Issues: Top challenges, and opportunities facing the insurance industry in 2024

- LinkedIn: Impact of System Integration for your Business Operations, 2023

- O’Reilly, Data Quality Fundamentals, 2022

- Harvard Business Review

- Disjointed Software Dilemma, Medium, 2023

- Penalties for Violating HIPAA, ADA

- Kepler Cannon Analysis

Read More

The Open Book on Compliance – US Open Banking Regulations Decoded

The CFPB’s new Open Banking regulations will impact how financial service providers can access and monetize consumer data, while also influencing future practices around security, consent, and data sharing.

Mixed Reality

As these technologies become more accessible to the wider public, AR and VR are expected to grow into a $125 billion market by 2025.

Money Games

The use of gamification has proliferated across all industries, with retail, entertainment and education leading the charge. Apps like Duo Lingo, Kahoot, Fitbit, Starbucks etc., are all some of the most prevalent examples.

Monetizing Data Analytics

For several years, it has been said that “data is the new oil” and arguably, the most valuable strategic asset for a business. Whilst getting value out of data might be less straight-forward, it is true that data needs to be refined to make it valuable.

From Cards to Chains – Payments in the Blockchain Era

To remain competitive in the evolving financial landscape, card networks are uniquely positioned to bridge this gap between traditional payments and new blockchain networks as transaction facilitators, leveraging their global reach to make transactions on their networks quicker, cheaper, and more secure.

A Borderless World

Significant shifts are underway in the cross-border payments sector, across the demand-side and supply-side. Consumer expectations from domestic payments (instant, fully traceable, risk-free, etc.) are being applied to the more complex cross-border space. Businesses that capitalize on these shifts stand to shape the future of the industry.

Cracking the FedNow Code

Real-time payments are increasingly recognized as a critical component of modern financial systems, offering speed and convenience in an interconnected digital world. As we venture into the future, the recent launch of the Federal Reserve's instant payment service, FedNow, stands at the forefront of a payment revolution in the US.

Future-Proofing Healthcare Delivery

The right telehealth platform is critical to meeting patient expectations and providing the best possible provider, patient and administrator experience. Today patients are demanding more control over their healthcare and want to access care from anywhere.

The GenZ Wave

Gen Z is not merely a younger version of millennials; they are poised to disrupt all aspects of the economy. Companies must therefore adapt in time to cater to the preferences and expectations.

Gaming and Financial Services

As younger generations start to play for competition and skill development, there is a rise in payment flows, volumes, and subsequent opportunities arising out of the same. Financial institutions are not only presented with the opportunity to monetize on gamers but also target younger Gen Z and Millennial consumers to upsell and cross-sell their existing products.

Maximizing Value from Value Added Resellers

The role of Value Added Resellers (VARs) is transforming from basic reselling to strategic technology partnerships that offer comprehensive IT solutions. To maximize the value of these evolving relationships, firms must bring transparency to pricing, agreements, and the scope of work.

Latent Growth in LatAm Credit Cards

The payments industry has been experiencing explosive growth across Latin America over the past few years: cash usage has decreased ~20% as consumers pivoted towards payment products that are well integrated into the financial ecosystem.

Navigating the Buy Now Pay Later Era

The rising aspirations of consumers combined with the limited access to, and opaque nature of traditional financing solutions, has given rise to innovative products for underserved segments. BNPL is one such solution that offers short-term financing to users with the ability to pay in definite installments with low to no interest rates.

Modernizing B2B Client Delivery

Leading B2B firms are very well aware that their client delivery experience needs to have the same levels of service, responsiveness, transactional ease as any digital consumer experience. Majority (72%) of B2B buyers expect a similar experience on a B2B site as they get on a consumer website (1).

Winning in Mature Markets

Competition is an important facet of business world, and the process of seeking growth is a continuous one. One should never stop trying to win new customers or retain existing ones. After all, competitors are always trying to win your customers over, especially in mature markets.

Putting Customers At The Core of Your Business

Digital Transformation is about developing new capabilities and leveraging new channels to design and deliver a better client experience.

Realizing the Reality of Real Time Payments

Real time payment (RTP) transactions are likely to exceed 300B by 2023, growing at 40% per year worldwide. Financial Institutions need to quickly find their own space in this ecosystem. They must redefine their value proposition and rethink their business models around this phenomenon.

Client Loyalty 2.0

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

The Tale of Two Countries – Insurance

The pandemic has created unprecedented challenges for the insurance industry. Experiences of the world’s biggest economies (U.S. & China) offer valuable lessons as to where the industry can improve and change in order to better handle similar events in future and build sustainable risk management systems.

Path to Innovation

Innovation has been in vogue for over a decade but the need to be innovative has never been felt as strongly as today. As businesses are learning to thrive under the lasting effects of the pandemic, they need to reinvent products, services and customer experiences to satiate emerging patterns of demand. To truly capitalize on the opportunity, business leaders need to look beyond internal capabilities and embrace a networked model of innovation to drive positive impact.

Reimagining Marketing

The COVID-19 pandemic has re-shaped the landscape for marketers. They are not only forced to cut budgets to save costs, but also face the challenge of keeping up with new emerging customer behaviors. These unprecedented changes call for a broader shift in marketing tactics and investments to successfully navigate the current transformed landscape.

Age of Contactless Mobility

Cities are at a standstill, but they are bound to get moving again. Urban mobility will never be the same, and contactless payments will shape the new normal. Trends are shifting, preferences are being broken, and opportunities abound!

The Path to Decentralized Finance

We are on the cusp of a revolution within financial services that will have far-reaching ramifications for the +1 billion unbanked, current models of financial intermediation across entities and borders, and ultimately the very nature of how end-consumers understand financial health. As this understanding held by customers evolves, so too must the operations, services, and visions of providers.

An Agile Approach to Digitalizing Wholesale Banking

Credit has seen its fair share of ups and downs, from being the crux of financial services, to commoditization and mass distribution, to now being re-engineered. In the realm of Wholesale Credit, a revolution is underway.

Driving Productivity Through Systems Selection

Procurement often involves multiple disparate stakeholders, systems and protocol. This complexity results in increased reliance on inefficient sourcing processes and only partially takes advantage of all the benefits available from supplier competition.

Putting IT Infra Consumers on a Diet

One question seldom asked is “how do I put my (IT infrastructure) customers on a diet?” The demand side is often assumed as a given, and there is with little assessment of (over-) consumption by applications.

Smart Blockchain Contracts: Are We Finally Going Paperless?

Smart contacts offer the potential to facilitate or fully automate processes that are heavily paper-based today, particularly long-winded, expensive legal processes.

The Unbundling of Retail Banking

Not unlike a piece of software, retail banking can be portrayed as a stack comprised of 3 layers, where the complexity of each services can be abstracted into discrete segments and end products.

Binge-Worthy Digital Advice

While the trajectory of ‘digitization’ in financial services is encouraging, there is still significant demand from customers to expand and evolve their digital experience.